Sustainable Travel Trends for 2021

/I was interviewed for BBC Travel Show about predictions for sustainable tourism for 2021.

Here’s a deep dive into some details. (And here’s what we thought came to pass, and Sustainable Travel Trends for 2022 and 2023).

2020 had the biggest impact we’ve seen on travel, ever. In 2021 as a result we’re expecting to see sustainable tourism develop in a number of ways:

1. Growth of the Ethical Consumer

2. Increased Awareness of The Climate Crisis & COP 26

3. Advance in The Sustainable Development Goals by Travel

4. Progressively Green Government Policy

5. Industry Demand for Resilience

8. Upsurge in Consumer Demands for Responsible Tourism

10. Growing Wellness

11. Increase in Consumer Demand for Sustainable Tourism

12. Regenerative Travel Blossoms

13. An Appreciated Value of Sustainable Tourism

14. Backing for Sustainable Tourism

Never before 2020 have 100% of destinations been closed simultaneously. This has decimated not only 80% of the market (OECD) but community livelihoods and conservation funding worldwide. The World Travel & Tourism Council anticipates a 2020 53% drop in worldwide tourism jobs (174.4 million) and GDP ($4,711 billion).

Tourism was already dealing with crises: Climate Change and Biodiversity Loss. Now there’s Covid and a subsequent Recession on top. These all impact the sustainability triple bottom line, which is tourism’s capital – people, planet, profit.

The industry will bounce back in time, but it likely won’t be the same, in supply or demand.

Some Context…

In 2018, 87% travellers said they wanted to travel sustainably (Booking.com).

In 2019, over half (55%) of global travellers said they were more determined to make sustainable travel choices than the previous year.

But did they? No. We might have seen an increase, but it’s nothing like those numbers!

In 2020, when asked motivations for travel, sustainable standards come 25th, just +1 place on 2019 (BDRC annual holiday trends report).

Yet, BDRC research also shows sustainable tourism issues figure heavily in people’s trip desires for: safety (3rd worldwide), scenery and landscape (4th), friendly people (5th); history and culture and authentic local experiences (1st and 2nd respectively in Asia in 2018).

Basically, people want sustainability without really knowing that’s what it is and so demanding it.

Sustainability in tourism isn’t one thing. It’s a complex recipe of intangible services, brought together in often behind the scenes operations.

But consumers often want black/white easy answers, so often first focus lifestyle changes on ‘easy swaps’ in tangible products, if at all, not wanting to consider complex sustainability especially on holidays.

Governments largely haven’t stepped in with regulatory powers, rather siding with economy and letting market forces dictate and the private sector to self-regulate (excepting eg. beach closures).

As a result, sustainability in tourism has been created and driven by passionate individuals voluntarily and steadfastly committed to action simply as ‘the right thing to do’, like us and our worldwide partners at Earth Changers.

But without enough consumer demand specifically for more sustainable tourism, or government regulation stepping in, financial support is not forthcoming, resourcing and scale is a challenge and so it’s nothing like it could be, in value, volume or indeed the impact it’s set up to create.

But now Covid has given sustainable tourism a fast-forward of several years, to potentially the tipping point those of us who have worked to for years, but certainly never in this way expected:

1. Growth of the Ethical Consumer

Through Covid, consumers world over have come to better understand the difficult decisions and balance of economy versus society (health). In fact, this represents only 2/3 of the triple bottom line of sustainability, which also adds environment into the equation for a yet more complex decision-making.

• In April 2020, a UK government survey found only 9% of Britons wanted life to completely return to 'normal' after the first lockdown. People were able to notice cleaner air, more wildlife, stronger communities and valued food more - and liked it. They became increasingly aware that the health of people and planet are inseparable and it's time for change.

• Ethical consumer spending and finance reached record levels in 2019 (£98bn, UK, latest data, Ethical Consumerism in the Pandemic, Ethical Consumer/Coop, December 2020)

Food: Fairtrade sales increased 13.7% between October 2019 and October 2020. 28% of people plan to purchase Fairtrade in the future, compared to just 15% pre-pandemic.

Organic: sales increased by 19% in the 12 weeks ending May 20202; 19% of people intend to buy organic products after the pandemic, compared to 8% pre-March 2020.

Free-from: Meat-free and dairy-free product sales increased by 25% and 28% respectively in the 12 weeks ending April 2020. Going forward, 30% of people intend to eat less meat and dairy than before.

Plastic: Intention to reduce the use of single-use plastics is set to increase with 54% saying that they will be even more focused on this issue post-pandemic.

Local: 60% of consumers have said that post-pandemic they expect to buy from local shops (vs 40% pre-Covid).

Energy: 44% have reduced energy use during the pandemic, while 52% of people said they will be looking to reduce usage post-lockdown. 338% increase in spend on green electricity tariffs in 2019, up to £4.8bn.

Transport: 51% of people are using public transport less often than they did pre-Covid, Cautious over personal space; 16% of people still plan to avoid travelling with others in the future. 45% of people are interested in cycling or walking wherever possible post-lockdown and research shows a surge in demand for bicycles.

• In apparel, more than 3/5 consumers said brands’ promotion of sustainability was an important factor in their purchasing decision (McKinsey COVID-19 Sustainability in Apparel Consumer Survey, May 2020).

• 83% of Millennials believe it is important for the brands they purchase from to align with their values (5W Public Relations Report, Consumer Culture).

• Ethics is the 3rd most important factor in consumer purchase decisions (12.2%), after quality (36.5%) and price (35.7%), but ahead of convenience (8.7%), brand loyalty and individuality (1.7%): Consumers are more likely to prioritise sustainability over more convenient alternatives if the perceived value is there.(VeoWorld, 2021)

• In travel, Euromonitor International’s Voice of Industry Sustainability Survey found:

64% of global consumers want to travel sustainably + with a purpose (April 2020)

76% of consumers are expected to be more concerned about sustainability after COVID (July 2020)

Euromonitor International, Voice of Industry Sustainability Survey, April 2020

• When asked whether ‘sustainable tourism’ was more important to them than prior to the COVID-19 pandemic, 25% of the British public believed it was more so, versus 11% less: a net positive swing of 14% to sustainability. (BDRC, 2020)

2. Increased Awareness of The Climate Crisis & COP 26

The Covid pandemic has had interesting repercussions on the climate crisis.

2020’s COP 26 delay to November 2021, meaning an extra year of raising awareness: and a (2020) year of record-breaking global warming (again) and worldwide wild fires (again) wreaking havoc in the Amazon in Brazil, Australia and the US West Coast, amongst others. Public awareness of the impacts on lives and the dangers of the climate crisis to the planet is higher than ever.

• Euromonitor (Voice of Industry Sustainability Survey July 2020) found:

64% of global consumers are worried about climate change - yet only 50% of travel companies engage with SDG13 on climate change.

Consumers plan to decrease overall carbon emissions due to limited travel in the:

Short term 14%; Mid-term 48%; Permanent Change 21%; (No Change 10%, Not Sure 7%)

(How do we reconcile sustainable travel and climate change?)

Nationally Determined Contributions (NDCs): For COP26, as part of the Paris Agreement, countries were due to publish NDCs including emissions targets, climate policies and the regulations to deliver them. The year delay has now enabled countries to prepare the NDCs in the context of Covid19 crisis recovery, leading to more multi-faceted sustainability, people-centred and moral-obligation government policies to #buildbackbetter, such as incorporating working from home and the implications for public transport, which can reduce emissions.

• However, even with the postponement, only 75/197 countries have submitted their NDCs (as of publication in Jan 2021).

So we can expect to see a growing number, raising more awareness across the globe – although there is still a long way to go for many.

The US Election created further awareness with the huge difference to climate-denier Trump with Democrat Joe Biden’s plan for climate change and environmental justice, including his pledge to re-join the Paris climate agreement. Reversing Trump’s withdrawal as one of his first acts as president, this can make a huge difference to the world, US emissions and its transport and tourism policy, with a big push for electrification, Mr Biden is aiming for net zero emissions by the middle of the century.

• "With Biden's election, China, the USA, EU, Japan, South Korea - two thirds of the world economy and over 50% of global greenhouse gas emissions - would have [commitments toward reaching] net zero greenhouse gas emissions by mid-century… This could be an historic tipping point." - Bill Hare, Climate Action Tracker.

• The number of travel organisations pushing to address the Climate Crisis is growing.

In 2020, Earth Changers took part in the inaugural Climate Friendly Travel Think Tank, including much discussion of aviation and alternative fuels and concluded the climate crisis requires even more urgent action by entire global travel and tourism sector.

They’ve since seen their Climate Friendly Travel Registry for climate ambitions and Climate Friendly travel Diploma both launch and develop, to help scale tourism’s contribution.

We are seeing increased action by some – again those passionate, committed organisations who do so voluntarily.

In January 2020, Earth Changers joined Tourism Declares Climate Emergency: there are now 149+ signatories (at time of publication, January 2021).

We also joined the Future of Tourism coalition, whose 8th principle is “Mitigate climate impacts”, with 445+ signatories (at time of publication, January 2021).

3. Advance in The Sustainable Development Goals by Travel

Where Climate Change is SDG13, there are another 16 SDG goals to consider.

Earth Changers was developed from core for tourism for sustainable development.

We launched in the UN Year of Tourism for Sustainable Development (#IY2017), were an early accepted solution to sustainable tourism for development authorised in 2017 by the UN World Tourism Organisation, as the first tourism website to write in depth about the intersection of travel and the SDGs.

Now others in the sector are starting to pay attention – but not nearly enough, and even less than in other industries.

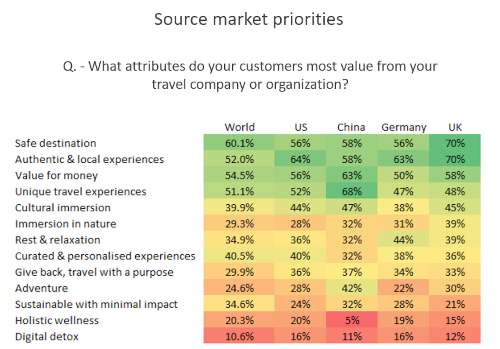

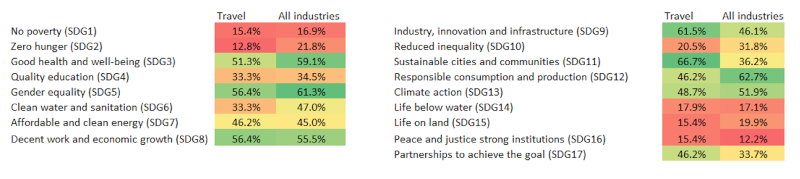

Travel Engagement with SDGs

Source: Euromonitor International – Voice of Industry, Sustainability Survey (July 2020)

In only 6/17 of the SDGs does the travel industry engage more than other industries on average:

SDG7: Affordable and Clean Energy

SDG8: Decent Work and Economic Growth (to be expected, given it mentions tourism?)

SDG9: Industry, Innovation and Infrastructure

SDG11: Sustainable Cities and Communities

SDG14: Life Below Water (to be expected, given it mentions tourism?)

SDG16: Peace, Justice and Strong Institutions

We should expect to see a lot more work on these, and for the other SDGs to level up in 2021, especially where tourism lags significantly:

SDG12: Responsible Production and Consumption – a 16% lag in a goal where tourism is specifically mentioned – although this has been a Covid challenge in 2020.

SDG2: Zero Hunger – 7% lag

SDG3: Good Health & Well Being – 8% lag

SDG5: Gender Equality – 5% lag, when travel is a predominantly female sector!

SDG6: Clean Water and Sanitation – 13% lag (to be expected, given it mentions tourism?)

SDG15: Life on Land – 4.5% lag, yet its assets are core to tourism, and it’s following the UN Decade on Biodiversity (2010-2020).

4. Greener Government Policy

To support commitments to the climate crisis and the Paris Agreement, and Agenda 2030’s SDGs, we are seeing more ambitious plans by country governments worldwide, including 65% of the world pledging net-zero targets (UNFCC, 2021). But will they actually deliver on pledges and how?

In 2020, the European Commission adopted their 5 year “Green Deal” sustainability focused environmental strategy, looking at strategy for Greenhouse Gas emission, energy, buildings, biodiversity, pollution, agriculture, mobility and circular economy.

During the COVID-19 pandemic, government policies have drastically altered lifestyles around the world. Borders were closed and populations confined to homes, changing energy demand, transport and consumption patterns. This drove the biggest annual fall in CO2 emissions since World War Two, a drop 2.4 billion tons of carbon or 7% - actually the amount we need to cut each year for the next decade.

Sadly, the emissions drop was temporary, already bouncing back to daily norms eg. in China.

But, Covid shows we can do it urgently when required. Will it continue for the urgent climate crises?

We expect more governmental support for sustainable tourism, mostly in the form of:

• Mobility: More cities will be made more friendly to cyclists and pedestrians, especially as more people will continue to work from home, along with greater support for electrifying transport: rail, buses, cars, and in tourism, coaches and sightseeing vehicles.

• Tourism Management over Marketing: Whilst Covid has shown the importance of tourism to destinations, it’s also highlighted (over-) dependence on tourism, for GDP and jobs. With overtourism still an issue despite, or because of, lockdowns (such as in Cornwall), we’ll see more movement to support communities and conservation in the right way through tourism, rather than just selling destinations.

• More Tourism Taxes

2020 was touted as being the year of the tourist tax, then the pandemic hit. We can expect it to pick up when travel returns.

Much of Europe which suffers overtourism now charges tourist taxes, famously including Venice, Amsterdam and the Balearic Islands. A fairly blunt instrument, taxes are one way governments and local authorities can choose to manage tourism.

Whilst often not high enough to put off visitors, they enable destinations to earn income towards paying for the huge public service costs of hosting them, but do not cover the enormous invisible burden (Travel Foundation, 2019) of excessive tourism cost to the environment, communities and culture.

Aviation is another area where greater tax may become a reality, because until alternative aviation fuels are available on mass, increasing flights will cause a negative environmental impact.

2021 will see the aviation industry voluntary CORSIA scheme (Carbon Offsetting and Reduction Scheme for International Aviation), limit emissions to a baseline of 2020 levels, thereafter offsetting carbon emissions growth from international flights – now a more ambitious target than expected given Covid!

Unlike car fuel, much international aviation fuel is tax exempt: Flight taxes tend to be departure taxes, income not usually used for environmental benefit. Aviation fuel taxes would follow the ‘polluter pays’ principle, and aim for a reduction in demand due to higher cost flights – especially if alternative travel options are available, such as rail, if price-comparable, potentially if better mobility policy is governmentally-supported.

A counter argument is that a fuel tax would not lead to fewer flights, rather a change in user (passenger/freight), thus only a modest impact on emissions and noise. With the impact of Covid already significantly reducing flights and passenger demand in 2021, and tourism revenues an economy support, governments may be less willing to consider aviation fuel tax.

• New Models of Tourism for Quality over Quantity

For years, tourist boards have been targeted with volume targets for the number of arrivals. This may have created economic growth through quantity, but it’s also the preserve of no-frills flights, huge cruise ships, and home rentals which don’t make for sustainable communities.

In 2021 we’ll see continue what’s already started as destinations seek new models of managing growth, and measuring tourism within that, like:

Amsterdam pursuing ‘Doughnut Economics’

Costa Rica considers its tourism impacts and management in the context of its Social Progress Index.

New Zealand has developed its Living Standards Framework of wellbeing outcomes and capital support.

As more and more destinations find their requirements no longer fit a purely capitalist economic growth agenda, we’ll see more switching to measuring tourism through different means, considering value over volume.

5. Industry Demand Resilience

The tourism sector is resilient. It always exists in constantly shifting sands of global situations, emergencies and customer hiccups, through which it has still grown unabated for decades, because people love to travel. For this reason, many travel organisations have actually been able to avoid considering sustainability.

But in 2020, there was no getting away from the need for resilience, without customers. And more of the non-sustainable tourism sector has come to realise that the strategies they need to pursue for resilience are exactly those for sustainability. Because sustainability is resilience, not a niche tourism type.

Survival is the name of the game for now. Those with deep wallets or low costs can be OK. Those with operations founded on debt and high liquidity may struggle in the face of lockdowns and border closures causing uncertainty and preventing travel sales.

In 2021, Coronavirus will continue to force unsustainable travel companies out of business with even big names like STA Travel failing.

6. Growth in Greenwashing

The rise in demand by consumers for sustainability and sustainable travel, and the rise in interest from the travel industry, will unfortunately almost inevitably lead to an increase in greenwashing.

It’s not that companies are always intending to manipulate; they may have the best of intentions – but as they say, “the road to hell is paved with good intentions”.

In the new-found desire to appear sustainable, many won’t know what they won’t know, and will make claims about sustainability purpose without actually being able to evidence those claims, or having reworked product to a sustainable supply chain and processes at core.

With consumers aware of the incidence of greenwashing, but unsure of its discernment, they will turn to specialist advisors able to guide them through the difference (like us!).

7. Rise in Certification

The travel industry’s increased interest in appearing and being sustainable, without necessarily knowing how to do so, will see a rise is sustainability certification and accreditation.

A journey of sustainability improvement is offered, helping organisations to step by step measure, monitor and improve their impacts.

Consolidation: With 150-200 sustainability certification schemes in tourism across the world, often specialising in different areas (geographical or tourism type), we’ll continue to see the rise of the Global Sustainable Tourism Council and those sustainability standards they ‘recognise’. To be (viably) sustainable themselves, no doubt some will merge.

Recognition: With so many tourism standards having historically lacked recognition from the trade let alone the consumer, certification hasn’t resulted in any marketing benefit. In 2021, with increased interest, and consolidation, standards recognition will grow in the tourism sector (and in future years, eventually the consumer public).

8. Upsurge in Consumer Demands for Responsible Tourism

In response to Covid, in 2021, consumers will demand more responsible travel, with companies who take responsibility for their business and impacts.

As we described in our blog, “Top Tips for Responsible Travel in the Covid Era: What Can We Expect in the New Normal?”, consumers will be expecting and offered to entice bookings:

Flexibility of booking terms – in case of Covid-disruption

Certainty: PCR tests and vaccination expectation will be commonplace, even integrated in time into health passports

Health support: Masks, sanitiser and touchless check-ins will all be made available.

The WTTC SafeTravels protocol and logo is a global standard for operating procedures.

Safety: Spatial distancing and personal space will be high on customer requirements; as will location space

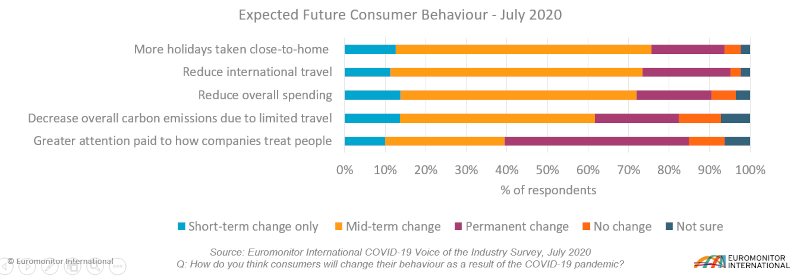

Shorter haul will initially be the necessity, but remain a preference for some even when pent-up demand is able to travel again:

94% consumers will take holidays closer to home:

+13% Short-term change; 63% Mid-term change; 18% Permanent change (4% No change; 2% Not sure)

+7.9% more consumers say they will reduce international travel permanently.

Connection: with authentic local people, culture and nature will be more important post-Covid.

Trust: always key to tourism sales, demand for responsible tourism – those who take responsibility for tourism – will be all the greater.

9. More Purpose in Tourism

Enabled by the industry better supporting the SDGs (see 3.), consumer demand will increase for purposeful travel with positive impacts. Unsure how to judge sustainable tourism, and wary of the rise in greenwashing (see 6.), they’ll look out for companies who have stepped up responsibility and can be judged by their past actions supporting communities and conservation, especially in the most troubling of Covid times - and not just for human lives,

“The pandemic has left local communities who protect wildlife struggling to make a living, and many threatened species increasingly exposed”

- Dr Bruno Oberle, IUCN Director General.

Species such as lions, giraffes and silverback gorilla became casualties of covid-induced poaching and the collapse of ecotourism and ranger jobs.

These are the type of organisations we work with at Earth Changers, who shifted priorities from Hospitality to Health, knowing their most important stakeholders are their local community.

10. Growing Wellness

With health, safety and personal responsibility on the up, so we will see an increase in wellness tourism, “travel associated with the pursuit of maintaining or enhancing one's personal well-being” (US non-profit Global Wellness Institute).

With the mass tourism sector representing ‘unwellness’ with its damaging model, for local people, places and customers, more consumers will turn to this form of responsible tourism for a real retreat from the unhealthiness of modern lives.

This may take the form of personal retreats, spas, meditation and yoga centres, activity breaks such as surf or hiking, or bootcamps and detox; and may range from a few classes to full-time immersion.

Most of Earth Changers’ global sustainable tourism partners incorporate wellness. Digital detox and get away to be at one with yourself and the natural world: in the Himalayas in India hike village ways, or in Nepal meditate on the majestic peaks, surf in Costa Rica, paddleboard in the Galapagos, horse ride through a biosphere in Croatia or try yoga on a rock on safari in Kenya…

11. Increase in Consumer Demand for Sustainable Tourism

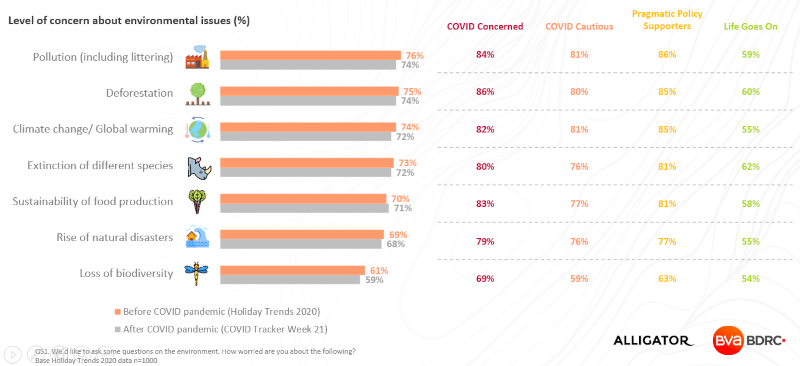

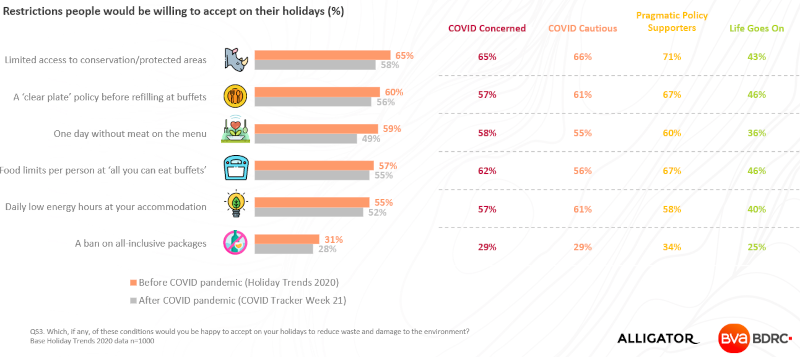

More Awareness of Sustainability: BDRC, who asked consumers about their level of concern about environmental issues before Covid and after its arrival, expected large drops as historic research would suggest that when one major issue dominates, interest in others significantly wanes. However, this was not the case, interest in each major sustainability issue tracked dropped just 1-2%.

The public display near-identical levels of concerns about the environment compared to before the pandemic:

Here’s how we expected the travel after coronavirus to play out into a ‘new responsible normal’ and the impacts on the SDGs.

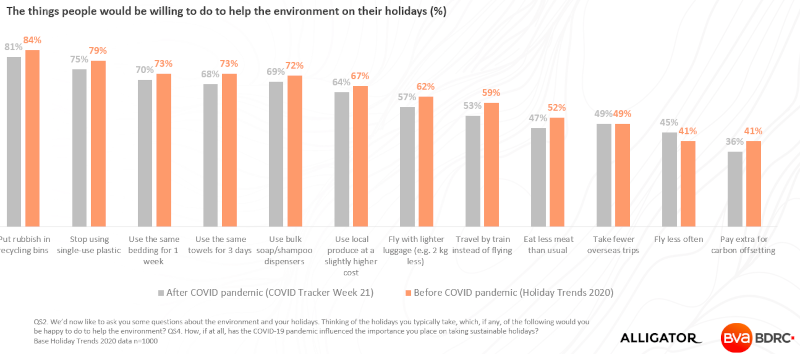

Holiday habits: Likewise, when asked what actions people would be willing to do to help the environment on their holidays, only small % drops were demonstrated, where in past years little willingness may have been shown at all:

Perhaps unsurprisingly when asked after the appearance of a global pandemic and a period of working from home, there was a small increase in willingness to fly less often, but only equal willingness to take fewer overseas trips: people don’t want to compromise their holidays, but will consider their sustainability – so long as their holiday experience isn’t restricted by it.

People are a little less willing to have their experience impacted by restrictions relating to sustainability:

Good news – sustainability in tourism doesn’t need to detract from holiday experience, if anything, it adds to its value! Here’s how and why: 8 Reasons to Book More Sustainable Tourism

“Britons are slowly coming to understand responsible tourism through connecting their travel motivations and concerns over environmental issues. Climate change and natural disasters are impacting the weather we might want to experience; the price we pay affects the quality of food we receive; safety is only paramount for responsible businesses; with deforestation, pollution, species extinction and biodiversity breakdown, we may not be able to see the scenery and landscapes we like; and if companies don’t behave responsibly to staff and locals, we won’t enjoy meeting friendly people. Making travel sustainable actually sits at the root of consumer influences and demand. Maybe after coronavirus, we will have more appreciation?” – Vicky Smith, Earth Changers, BDRC Holiday Trends 2020.

Faced with increased greenwashing due to the increased interest in sustainability, consumers will recognise they don’t know about how to discern what is sustainable travel and what’s not, and turn to specialists like us at Earth Changers to advise.

12. Regenerative Travel Blossoms

No sooner is the industry and consumers finally showing an interest in sustainability in tourism, then it’s time to think Regeneration – perhaps unsurprising after Covid19.

“Greener, smarter and less crowded. If sustainable tourism, which aims to counterbalance the social and environmental impacts associated with travel, was the aspirational outer limit of ecotourism before the pandemic, the new frontier is “regenerative travel.”

heralded the New York Times in August 2020.

Involving not just positive impact and sustainability, Regenerative Travel addresses many of the above trends to not only take responsibility for minimising the negatives of tourism, ensure the sustainability of people and places, and positively heal and impact them for the future, but importantly do it in a new holistic way, examining the systems change required – including (see 4.) new models and measures for tourism to help co-create ‘flourishing destinations’.

13. An Appreciated Value of Sustainable Tourism

Tourism value: With Covid, the value of tourism has been talked about more publicly worldwide. Long known in lesser developed countries to offer vital support to communities and conservation, the pause of tourism’s 10% global GDP and jobs has had a major impact in most countries, with the realisation it’s not just a leisure pursuit previously devalued as frivolous fun, but a powerhouse economic industry.

Sustainability Valued: Having missed travel, people have come to better value not just the economy and jobs it supports but consumers’ mental health, workers’ dignity, and the impacts on the enormous cross-sectoral supply chain. Tourism and its employees will be less taken for granted and more appreciated for the impacts on lives they facilitate.

Experience Valued: Consumers will look for more a differentiated experience with more value over volume, that doesn’t exploit but supports others, doesn’t damage but enhances the environment.

Expertise Valued: Throughout 2020 and Covid, consumers may not have been able to travel, but have had to postpone and cancel, and research destinations with new rules, regulations and protocols. Responsible tourism organisations who have offered and enabled flexibility, helped with changes, advice and support have been needed, and supported customers regardless of sales. Looking to more sustainable tourism in future, specialist expertise will be more valued and sought after than ever.

14. Backing & Green Finance for Sustainable Tourism

The above increasing demand for, desire to supply, and policies to back sustainability, including in tourism, with growing recognition and urgent need, will finally lead to an increase in much needed support for the sector.

Sustainable tourism suppliers and product are plentiful, and technology abounds in tourism. The hindrance to sustainable tourism growth has been slow consumer demand, thus ROI, and consequent investment and support.

But the sector is far from without resource: land, water, biodiversity, carbon are all valuble ecosystem services, assets, and nascent credit - or offset - markets. Value will be driven by reported and verified results, and become not only more appreciated (13.) to experience, but also these are the tradeable assets of the future and the business case will strengthen.

From the fallout of Covid19, growth in demand and urgency for sustainability, we can now start to see emerging financial and resource support to bring the existing sustainable tourism product and expertise together with existing technology to scale - and scale positive impacts. It’s time for governments, investors and consumers to put their money where their mouth is, as they turn away from unsustainable options in favour of green finance for sustainable and regenerative tourism.

Never before has sustainable tourism been so important and had such opportunity!

In fact, it’s the opportunity of the industry’s lifetime for wholescale change to greater sustainability.

We’re optimistic - may 2021 be filled with positive, regenerative impacts!

[How well did we do and what’s next? Check our Sustainable Travel Trends for 2022]

Let us know what you think…